Portfolio projections is a feature on the platform that simulates for a client account, a distribution of future portfolio performance in good, average and poor market outcomes. These projections are based on the cash flows and the asset class makeup of the portfolio, and can be simulated at a client account or individual portfolio level.

To project the portfolio performance chart, the algorithm performs a statistical simulation through stochastic random sampling via a method called the Monte Carlo simulation. Monte Carlo simulations are a highly regarded tool to obtain an array of results for a statistical query, from a large dataset consisting of thousands of data points.

The simulation model produces thousands of projections of plausible future states, taking into account Mason Stevens’ view on assets, expected returns and implied volatility to predict future portfolio performance.

The values displayed on the simulated graph are not to be relied on as the exact portfolio or account values at the end of the period. Various factors such as fees and taxes will also influence the outcome based on the type of product being simulated.

The process begins with an initial value of the portfolio. The value then grows and shrinks in each rebalance period (e.g. quarter), in each of the simulation paths, based on returns, contribution and withdrawals applied. The algorithm rebalances the entire portfolio to realign the weights after considering the returns and cashflows realised in that particular simulation path. For example, if the rebalance frequency is quarterly, then after every quarter the portfolio weights will match the original weights.

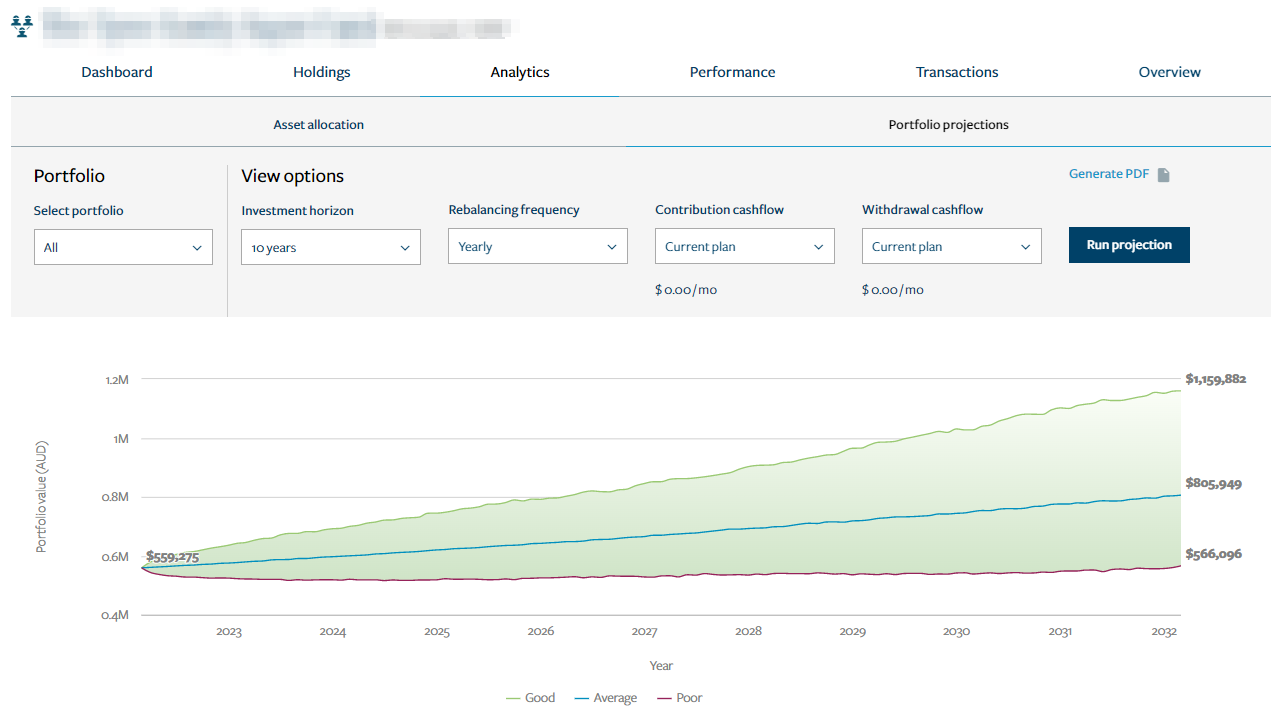

The results are summarised in a projection chart, as above, which shows good, average and poor outcomes based on the algorithms 10th, 50th and 90th percentile. This means the good path will only have 10% of returns with lower values than the predicted return while the poor path will have 90% of returns with lower values.

The algorithm relies on four key date inputs prepared by the Mason Stevens economics team, based on their view of investment markets and future volatility. The four key inputs are:

- Asset classes

- Expected return (gross of fees and any taxes)

- Implied volatility

- Correlations between the asset classes under review

Asset Class

The asset classes are based upon current platform model:

- Australian equity

- International equity

- Domestic cash

- Australian fixed income

- International cash

- International fixed income

- Property

- Multiclass (unused)

- Infrastructure

- Alternative & Other

Expected returns

Expected returns are a proprietary combination of Mason Stevens’ Investment Committee views, as well as historical statistical analysis, using geometric mean (averaging).

Implied Volatility

Implied volatility is a measure of the asset class sensitivity to fluctuations in prices through a normal market environment. A higher implied volatility implies a higher probability that the investment security, index or asset class will change in value, over the given time frame. Conversely, a lower implied volatility implies the opposite. This data is available through various financial derivative instruments – such as options, futures, swaps and forward – that allow Mason Stevens to assess the implied volatility for each asset class under review.

Correlations

We analyse rolling correlations that are updated periodically in order to assess relationships with each asset class. For example, the correlation between Australian equity and international equity. In analysing this relationship, correlation data will highlight that for an incremental change in value of international equities, how much Australian equities would change in value relative to the international equities. The results are a continuum from -100% (inversely correlated) to 0% (uncorrelated) to +100% (perfectly correlated).

The portfolio projections are made using various assumptions of risk and return, volatilities and correlations that may or may not eventuate or persist and may not be factored into projected market prices.

While the input data is updated periodically, there is significant probability that expected returns may deviate due to changes in market prices and valuations, geopolitical and environmental events, changes in taxation and international taxation treaties, central bank market intervention, foreign currency exchange rate fluctuations and various other factors affecting financial instrument valuations.